Citation: Beddoes C, “Understanding the Market for Wearable Larege Volume Injectors”. ONdrugDelivery Magazine, Issue 70 (Sep 2016), pp 4-7.

Clare Beddoes gives an overview of the exciting state of the injectables market, with a particular eye towards the new sector of wearable bolus injectors, also known as large volume injection devices.

The injectable drugs and devices market is a dynamic and exciting sector to be involved in, and remains a healthy one. Globally, this market is continuing to grow, with recent forecasts estimating a compound annual growth rate (CAGR) of 13.2% over the next 10 years to reach approximately US$824 billion (£616 billion) by 2025.1

There are, of course, many different devices available to deliver injectable drugs, with new types being launched all of the time. Furthermore, many of these devices have been – or are being – developed specifically for patient self-administration. There are many factors driving demand for these devices, most of which have been written about before.

“What will the addressable market for these LVI devices actually be? How many of the biologics coming through the pipeline will be formulated for SC delivery? How many of those SC formulations will be launched to market at volumes >2 mL?”

Wearable bolus injectors, also known as large volume injection (LVI) devices, represent a new and innovative sector within the injectable drug delivery market. They provide the opportunity to deliver large (>1-2 mL) volumes of drugs subcutaneously together with the many associated benefits this offers to drug developers, clinicians and patients.

Biologic therapeutics typically require parenteral (i.e. intravenous (IV), subcutaneous (SC), intramuscular (IM)) delivery, and high volumes per single dose are often needed. This particular group of drugs is growing; one-third of annual drug approvals are of biologics and there is a healthy pipeline of over 900 biologics in development.2 It is this growth in the biologics market that is thought to be one of the key drivers that will forge the emergence of LVI devices.

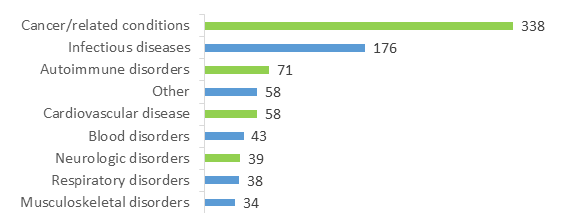

The size of the market opportunity for LVI devices alone has been estimated at $8.1 billion by 2025, with over 50% of this driven by devices to deliver drugs for cancer and related conditions,3 and indeed the biologics pipeline is dominated by oncology drugs (Figure 1).

Much is written about the market need for LVI devices, not only for delivery of high volumes, but such devices are also seen as a means of extending the lifecycles of drugs nearing the end of their patent life by, for example, reformulating from IV to SC.

But what will the addressable market for these LVI devices actually be? How many of the biologics coming through the pipeline will be formulated for SC delivery? How many of those SC formulations will be launched to market at volumes >2 mL? And what should LVI device companies focus on during development, to meet the requirements of the drug, the pharma companies and – perhaps most importantly – the patients?

It is of course not possible to predict accurately which drugs currently in development will be formulated for SC delivery in volumes requiring an LVI device. However, if we respond to predictions and focus for now on cancer, there are many challenges that device developers could face when considering a suitable solution, especially working on the premise that LVI devices are ultimately intended for patient self-administration of therapeutics.

This article doesn’t claim to have all of the answers but aims to pose questions which will provoke thought, discussion and perhaps generate proposals for potential solutions.

IS CANCER THE REAL DRIVER?

The global burden of cancer continues to increase as the world’s population grows and ages. In 2012 there were an estimated 14.1 million new cancer cases and 8.2 million cancer deaths, as opposed to 12.7 million new cancer cases and 7.6 million cancer deaths in 2008.5 Which cancers, disease stages and associated therapies and, of course, patients would actually be applicable to LVI devices? The majority of injectable cancer therapeutics are currently administered IV and many have potentially serious side effects for which close hospital monitoring is required. How many of those could be reformulated to SC format? How many would be suitable (safe) for a patient to self-administer at home and realistically how many SC oncology drugs would need an LVI device to enable self-administration?

There are several drugs for cancer and associated conditions that are already available for SC delivery, but most are currently indicated only for use within, or treatment initiated within, a healthcare setting. In several cases this may well be because a suitable drug and delivery device combination for self-administration is not yet available, but if there were, what type of cancer patients would be appropriate candidates to administer their own cancer therapeutic outside of a healthcare setting? What profile of cancer patients would be willing to self-administer an injectable oncology drug at home? What are the attitudes of oncologists to sending patients home to self-administer (often very expensive) drugs?

“There are many other therapeutic areas beyond cancer with drugs either on the market or in development, which may be applicable to LVI devices…”

During the early stages of cancer, or as a result of successful treatment and ongoing management of the disease, many cancer patients could be described as otherwise well, wishing to continue with normal life as much as possible. This wish is often hindered by regular, and often lengthy, trips to a healthcare setting for treatment, constantly reminding patients of the burden of their disease, and often associated with negative psychological effects. Therefore, an alternative means of drug delivery, allowing quicker treatment, is a clear benefit to those patients.

This certainly appears to have been in part, the premise behind Herceptin SC (subcutaneous trastuzumab) from Roche (Basel, Switzerland), which is in clinical trials in an LVI device. Although the marketed product is currently still only administered within a healthcare setting using a syringe, it has been shown to save significant time – taking just 2-5 minutes to administer 5 mL subcutaneously, as opposed to 30-90 minutes IV, for the same therapeutic benefit. Those time saving benefits are also seen with Mabthera SC (subcutaneous rituximab), the second of Roche’s mAbs to be made available as SC formulation, allowing a 11.7 mL therapeutic dose to be administered in 5-10 minutes compared with 2.5 hours for standard IV delivery.

It is worth noting that the speed with which 5 mL and 11.7 mL can be delivered and tolerated by patients is made possible by co-formulation of the drugs with the excipient of recombinant human hyaluronidase technology – also known as EnhanzeTM – from Halozyme Therapeutics (San Diego, CA, US). The excipient technology removes the traditional limitations on the volume of drugs and biologics that can be delivered subcutaneously6 by effectively (and reversibly) degrading hyaluronan – a component of normal tissue – thus allowing the drug to disperse into the “space” and not simply leak back out, or cause local oedema and pain during injection. Many pharma companies have signed deals with Halozyme for access to this technology.

Currently, like Herceptin SC, Mabthera SC is delivered via hand-held syringe by a healthcare professional (likely a nurse), who administers the injection by simply holding the syringe in place for the required amount of time.

Could patients tolerate self-injecting large volumes using a standard syringe over several minutes? And what of large volume SC drugs not co-formulated with an excipient such as EnhanzeTM? How long would it take to administer 5 or even 12 mL of drug? Will these factors drive demand for wearable LVI devices capable of delivering a drug over a longer period of time, whether for use within the clinic or home setting?

What of patients with cancer at a later stage who are likely to be receiving a combination of different therapeutics, may require periods of hospitalisation for that therapy and thus may well be receiving many of those drugs IV? Would a patient receive some drugs intravenously and others subcutaneously if available in an LVI? Would that provide any efficiency in a hospital setting?

There is increasing focus on combination therapies for cancer and this seems set to continue with the growing interest in immunotherapeutics. At the recent ASCO 2016 conference in the US, much data was presented on studies combining treatments. Indeed drug company executives told Reuters there is increasing “focus on how best to combine therapies to attack multiple mechanisms of the disease, determine which patients are most likely to respond to them and how long patients will likely need to be treated”.7 So what of LVI in this context?

Oncologists we speak to seem a little hazy about this too. When it comes to the question of using SC drugs as monotherapy, but administered in the healthcare setting, the advantages associated with significantly quicker SC delivery seem clear: “It is more convenient for the patient and nurse, it is more cost effective.” However, when an SC drug would be used in combination with IV drugs, opinion can be conflicting: “It is convenient even with IV chemo,” versus “Time saving is key – but if patients are also receiving IV drugs there is no real benefit and it wouldn’t make sense to give the SC version.”

It seems, then, the practice of treating cancer is set to get even more complicated, and with combination therapies being developed and advanced, possibly even for early-stage disease, the scenarios in which the use of LVI in oncology will be considered are also set to increase in complexity.

IT’S NOT JUST CANCER THOUGH

There are many other therapeutic areas beyond cancer with drugs either on the market or in development, which may be applicable to LVI devices (including biologics, see Figure 1). Many questions also come to mind for other conditions such as autoimmune (AI), cardiovascular and neurological diseases.

Autoimmune

Many of the SC injectable drugs/biologics already on the market for AI conditions such as rheumatoid arthritis and multiple sclerosis are available in volumes of 1-2 mL, i.e. capable of delivery by standard syringes, pen injectors, auto injectors etc. Therefore, this is the market in which future SC therapies will have to play.

Figure 1: Biologic medicines in development by therapeutic category (some medicines are listed in more than one category).4

Would there be any benefit to having a large volume drug, or will efforts be made to formulate to volumes similar to those that competitors have already achieved and thus be made available in injection devices, with which many patients living with these conditions are already familiar?

Or could there be an opportunity to “roll-up” doses so that patients would have to self-administer drugs less often via use of a larger dose in a larger volume? i.e. reducing injection frequency and potentially the feeling of disease burden that more regular dosing can impose.

Cardiovascular

2015 saw a battle to be first to market with a new class of drug – a monoclonal antibody (PCSK9 inhibitor) injection –- for reducing cholesterol in patients with certain conditions that aren’t responding to statins.

One such therapeutic, Repatha (Amgen), was launched in August 2015 as 140 mg every two weeks or 420 mg once monthly. The monthly treatment regimen involved three lots of 1 mL injections, using either prefilled syringes, or three lots of the SureClick auto injector. However, in July this year the US FDA approved a wearable injector – called the “Pushtronex” system to deliver the 420 mg (3.5 mL) monthly dose. Pushtronex is based on the Smart Dose technology platform of West Pharmaceutical Services. The device has been available in the US since August 2016 and it will be interesting to watch what happens with competitor drugs.

Neurological

Neurological disease is an area that still has massive unmet therapeutic need, for conditions such as Alzheimer’s and Parkinson’s.

The blood-brain barrier (BBB) causes great challenges, potentially limiting successful drug development in this field and may push the drug volumes required to confer therapeutic benefit beyond those capable of delivery by standard SC devices.

Will successful drugs to treat neurological disease be launched (initially at least) in large volumes – to be able to elicit a therapeutic effect – and thus require large volume injection?

“…it’s a young, dynamic, exciting and highly innovative sector which holds great potential to change patients’ lives radically and is one to watch very closely indeed…”

What groups of patients would be applicable? For example, many drugs currently in development for Alzheimer’s are focused on treating early-stage disease, or those at high risk but pre-symptomatic. If indications are expanded beyond those with symptomatic disease, could LVI be used by patients with more advanced Alzheimer’s symptoms? Would such a group tolerate a wearable device? What user experience issues would have to be given careful consideration?

BALANCING THE BOOKS

Then there is the issue of reimbursement. Who will pay for LVI delivery devices? What health economic evidence will those payers look for before accepting drug-device combinations into formulary and common practice? Despite studies suggesting that developing, or reformulating, biologics to SC, or even intramuscular, versions has the potential to lower healthcare administration costs,8 this appears to depend on the healthcare system.

Back to cancer as an example; in the US SC forms of the mAbs Herceptin and MabThera are not yet available. This may well be because the patents in the US have not yet expired – they are due 2019 and September 2016, respectively – whereas they have already passed in, for example, Europe. However, talking to oncologists in the US reveals that some are not actually aware of the SC formulations of those well respected drugs, and if they are, they are often dismissive about the possibility of being able to use them in the US, certainly in the healthcare setting they are currently approved for, due to the way the reimbursement system currently favours IV over SC drugs.

For example, a leading US lymphoma oncologist told us: “There may be a financial barrier to SC [versions of these oncology drugs]. Oncologists in private practice are reimbursed for every IV infusion they give and so SC would be a huge economic disadvantage for those clinics.” Whilst an experienced US breast cancer oncologist stated: “I am not sure why Herceptin SC is not available here, but it is potentially due to the fact that private practice can charge more for IV infusion.”

It is unclear whether those are isolated views or facts which highlight barriers that payment models could pose to widespread uptake of future SC oncology drugs in the US – and elsewhere – and whether this differs for SC drugs intended for use within a clinic or for self-administration.

In Germany, a fairer reimbursement system is also being called for as some feel the current one is limiting the number of patients who receive SC formulations of oncology therapies due to economic reasons for the prescribing centres involved. It is believed that SC (and oral therapies), which still require medical staff to provide time-consuming services e.g. patient consultations, and monitoring of side-effects, are not adequately reimbursed.

As a result, in 2014, SC Herceptin accounted for only 14% of the total amount of trastuzumab administered in Germany, compared with 60.1% in the UK and 76.4% in Sweden, over the same period.9 These data obviously reflect the situation for use of SC drugs within the healthcare setting and was gathered before any SC oncologic therapies are being selfadministered in the home setting, and so it is not yet clear how current reimbursement models would affect any switch of location of cancer treatment.

Yes, there are many questions raised in this article (and potentially still to be answered) about this market sector, but what is clear is that it’s a young, dynamic, exciting and highly innovative sector which holds great potential to change patients’ lives radically and is one to watch very closely indeed.

REFERENCES

- Global Injectable Drug Delivery Market Analysis & Trends – Industry Forecast to 2025, http://www.researchandmarkets.com/research/cpvnp9/global_injectable

- Medicines in development – Biologics http://phrma.org/sites/default/files/pdf/biologics2013.pdf

- Bolus Injectors Market, 2014-2024, November 2013 – Roots Analysis Private Ltd

- Biologics – 2013 Report phrma-docs.phrma.org/sites/default/files/pdf/biologicsoverview2013.pdf

- GLOBOCAN 2012: Estimated Cancer Incidence, Mortality and Prevalence Worldwide in 2012

- www.halozyme.com/technology-and-products/enhanze/default.aspx

- US regulator says too many drugmakers chasing same cancer strategy uk.reuters.com/article/us-health-cancer-fda/u-s-regulator-says-too-many-drugmakers-chasing-same-cancer-strategy-idUKKCN0YW15T

- Tetteh K, Morris S, “Evaluating the administration costs of biologic drugs: development of a cost algorithm”. Health Economics Review, 2014, Vol 4, p 26.

- Jackisch C et al, “Subcutaneous Trastuzumab for HER2-positive Breast Cancer – Evidence and Practical Experience in 7 German Centers”. Geburtshilfe und Frauenheilkunde, 2015, Vol 75(6), pp 566-573.